Comprehensive Energy Data Intelligence

Information About Energy Companies, Their Assets, Market Deals, Industry Documents and More...

$3 Billion Deal, Marathon Oil Buys Ensign Natural Resources

11/16/2022

A $3.0 billion cash definitive agreement to purchase the Eagle Ford assets of Ensign Natural Resources has been concluded by Marathon Oil Corporation. The transaction is subject to customary terms and conditions, including closing adjustments, and is anticipated closing by year-end 2022, according to the company press release on November 2.

The transaction is considerably accretive to Marathon Oil's key financial metrics without delay, anticipated driving a 17% increase to 2023 operating cash flow and a 15% increase to free cash flow. The transaction was acquired at about 3.4x 2023 EBITDA and a 17% free cash flow yield, accretive relative to Marathon Oil's 2023 stand-alone metrics at the same price deck (4.7x EV/EBITDA, 13% FCF Yield).

As the transaction is accretive to Marathon Oil's cash flow profile, it will improve shareholder distributions, consistent with the company's transparent Return of Capital Framework that is solely driven by operating cash flow and, in a $60/bbl WTI or higher price environment, calls for not less than 40% of annual operating cash flow to be returned to equity holders.

To get deeper, Marathon Oil expects the transaction to increase 2023 shareholder distribution capacity by practically 17%. Additionally, due to the cash flow accretive nature of the transaction, Marathon Oil expects to raise its quarterly base dividend an additional 11% post transaction close to 10ct/sh. Marathon Oil still considers achieving its aim to take back at least 50% of adjusted operating cash flow to shareholders, outperforming its 40% framework minimum.

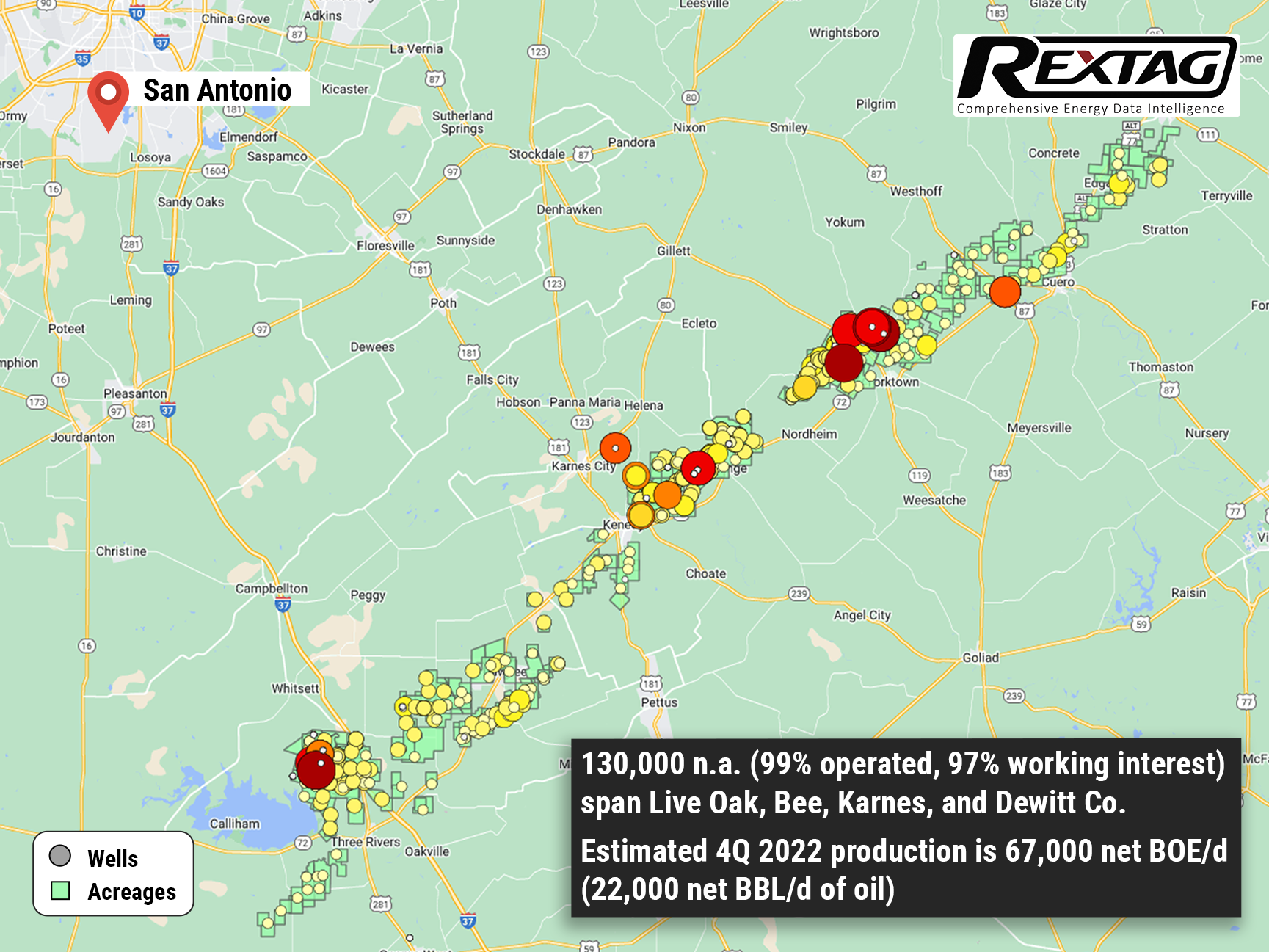

This transaction considerably improves Marathon Oil's Eagle Ford position through the addition of 130,000 net acres with 97% working interest situated mainly in the prolific condensate and wet gas phase windows of the play. The company considers acquiring more than 600 undrilled locations, representing an inventory life greater than 15 years, with inventory that immediately competes for capital in the Marathon Oil portfolio.

The acreage is adjacent to Marathon Oil's existing Eagle Ford position, letting the Company leverage its knowledge, experience, and operating strengths in the Basin, while raising its Basin-scale to 290,000 net acres and facilitating optimization of supply chain accessibility, and contributing to cost control in a tight service market. The acquisition also includes 700 existing wells, most of which were completed before 2015 with early-generation completion designs. These existing locations offer upside redevelopment potential, none of which was considered in the Company's valuation of the asset or inventory count.

The 130,000 net acres (99% operated, 97% working interest) Marathon Oil is purchasing from Ensign Natural Resources span Live Oak, Bee, Karnes, and Dewitt Counties across the condensate, wet gas, and dry gas phase windows of the Eagle Ford. The estimated fourth quarter 2022 oil equivalent production is 67,000 net boed (22,000 net bopd of oil). Marathon Oil supposes to hold its fourth quarter production flat with virtually 1 rig and 35 to 40 wells to sales per year.

The Company's valuation of the asset was based on this maintenance-level program and does not have any synergy credits or upside redevelopment opportunities. The transaction is expected to be closed by year-end 2022 with an effective date of October 1, 2022. Purchased tangible assets are eligible for full expensing for the purpose of income tax optimization.

Morgan Stanley is serving as the lead financial advisor to Marathon Oil and is providing committed financing to Marathon Oil with respect to a portion of the purchase price. White & Case LLP is serving as outside legal counsel for Marathon Oil.

Evercore and J.P. Morgan Securities LLC are serving as financial advisors to Ensign Natural Resources. Sidley Austin LLP is serving as the principal legal advisor to Ensign Natural Resources.

If you are looking for more information about energy companies, their assets, and energy deals, please, contact our sales office mapping@hartenergy.com, Tel. 619-349-4970 or SCHEDULE A DEMO to learn how Rextag can help you leverage energy data for your business.

Lime Rock Resources Starts the Year With a Bang — a Money Bang!

![$data['article']['post_image_alt']](https://images2.rextag.com/public/blog/Lime RockResources-Starts-the-Year-With-a-Bang-a-Money-Bang.png)

Still waters run deep: after patiently waiting for 2 years, Lime Rock Resources starts the year with a pair of acquisitions worth $358.5 million The two acquisitions include Abraxas Petroleum’s Williston Basin position in North Dakota: about 3,500 acres of land and 19,400 boed of net production, as well as properties situated in Burleson, Milam, and Robertson in Texas from a third party, that contain 46,000 contiguous net acres and produce 7,700 boed as of the closing of the deal. The company intends to intensify its focus on low-risk opportunities and margins, which will significantly boost Lime’s market position going further.

Ensign’s Assets Are Acquired by Marathon for $3 Billion

![$data['article']['post_image_alt']](https://images2.rextag.com/public/blog/111Blog_Marathon_Completes_Ensign_Eagle_FordAcquisition_12_2022.png)

Marathon Oil Corp. closes the acquisition of Ensign Natural Resources’ Eagle Ford assets for $3 billion cash, according to the company’s release on December 27. The purchase includes 130,000 net acres (99% operated, 97% working interest) in acreage adjacent to Marathon Oil’s existing Eagle Ford position. Ensign’s estimated fourth-quarter production will average 67,000 net boe/d, including 22,000 net bbl/d of oil.

![$data['article']['post_image_alt']](https://images2.rextag.com/public/blog/297_Blog_Keystone XL Pipeline Controversy and Wildlife Disaster From Trump's Green Light to Biden's Red Light on the 15 Billion Project.jpg)

The pipeline industry in the USA faced and still faces a range of regulatory challenges, including permitting delays, environmental requirements, and public opposition to pipeline projects. In recent years, pipeline projects like the Keystone XL and Dakota Access pipelines had legal and regulatory obstacles that delayed or canceled their construction. Keystone XL Pipeline, proposed by TransCanada in 2008, aimed to transport crude oil from Canada (around Calgary and Edmonton) to refineries on the Gulf Coast (Port Arthur). The project faced opposition from environmental groups and indigenous communities, who argued that it would contribute to climate change and pose a risk to water resources. In 2015, President Obama rejected the project, citing concerns about its environmental impact. However, in 2017, President Trump revived the project, leading to further legal challenges. In June 2021, U.S. President Joe Biden officially canceled the project on his first day in office.

![$data['article']['post_image_alt']](https://images2.rextag.com/public/blog/282_Blog_Renewable Natural Gas How RNG Changes the Industry.jpg)

The renewable natural gas (RNG) industry in the United States is showing promising signs of growth. As of 2019, the U.S. consumed 261 billion cubic feet (BCF) of RNG, primarily utilized by independent power producers, electric utilities, and various commercial and industrial entities. However, this figure represents only a small fraction of its potential. Research indicates that the U.S. could theoretically produce up to 2,200 BCF of RNG through anaerobic digestion alone, which would equate to about 11% of daily national natural gas consumption.

![$data['article']['post_image_alt']](https://images2.rextag.com/public/blog/295_Blog_Renewable Efforts Lag as Global Oil and Gas Demand Continues to Rise.jpg)

Recently, the progress toward an energy transition is hitting a snag. Sales of electric vehicles are decelerating, and the growth in wind and solar power needs to be keeping pace with expectations. To make matters more challenging, electricity prices are climbing when they were expected to fall. Amidst these setbacks, the oil and gas sectors are proving resilient. According to BP's latest energy outlook, not only are these energy mainstays here to stay, but their demand is expected to remain relatively high even after reaching a peak. Interestingly, BP forecasts that oil demand will reach its zenith next year, marking a critical moment in energy consumption trends. This isn't the first time BP has projected a peak in oil demand. Back in 2019, their review anticipated a decline in demand growth, but the prediction fell flat. Instead, oil demand surged to unprecedented levels following the end of the global pandemic lockdowns, defying previous forecasts and underscoring the enduring dominance of traditional energy sources in the global market.