Comprehensive Energy Data Intelligence

Information About Energy Companies, Their Assets, Market Deals, Industry Documents and More...

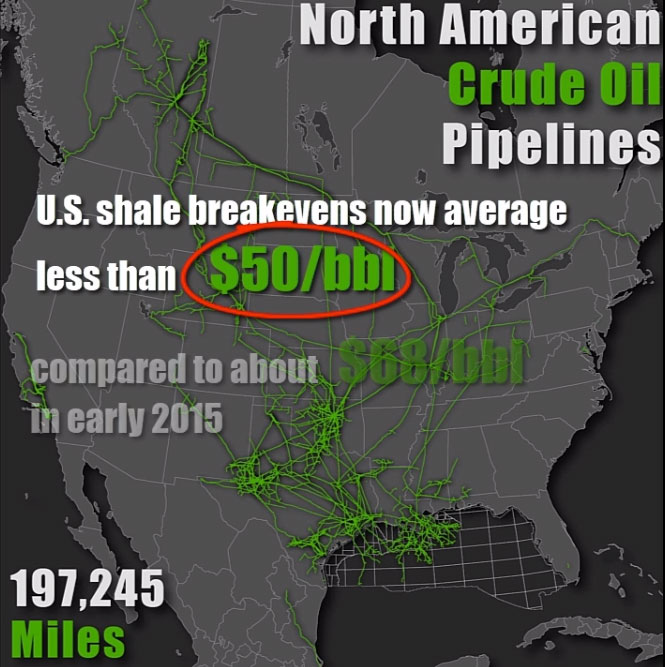

U.S. Crude Breakevens at Less Than $50/Bbl - Pipelines Help

03/04/2018

Oil and gas sector continues to restore its growth trajectory in 2018. Growing and more stable crude price outlook helps. However, this is not the only key to the industrial success.

OPEC remaining relevant a strong market player was influencing prices last year and will do so in 2018 as well. Its 30 million barrels share of the world market makes it a power to consider. They’re a big player and will continue to have a big influence on the market in years to come.

OPEC and Russia in their joint effort to cut production since end of 2017 succeeded and helped rebalance the market significantly. Production cuts by about 1.8 million barrels per day had an uptick effect on oil prices ever since. Oil prices—also aided by rising global demand—have steadily risen from the low $40s/bbl in 2016 to about $64/bbl in 2017.

U.S. shale breakevens now average less than $50/bbl, compared to about $68/bbl in early 2015, according to Deloitte.

This encouraging trend comes to view despite the inflationary trend which the industry has felt since the sector returned to growth in 2016. So, there must be some serious steps have taken to still be able to produce yet cheaper than before to overcome inflation.

Key reasons are TECHNOLOGY IMPROVEMENTS.

Essentially, DIGITAL SOLUTIONS is the success factor. usage of production data is, though still limited, becomes more systematic in nature. In upstream, producers have learned to differentiate the well-performing wells from the rest. Data on these field champions brings great insights about technology to apply to less successful areas. Thus, companies are using digital technologies to enhance their field development.

Additionally, SUPPLY CHAIN improvements help. Midstream companies having received significant investments prioir to the 2014-2016 price downturn times, still feel a significant debt burden. They are also slow to increase returns on investments made. All this has made midstream companies less attractive in the eyes of investors as oil prices began rebalancing.

This left transportation companies with no options left but improve their efficiency. Growing (even booming in Permian) Lower 48 production has put additional pressure on midstream operators. 2018 has become a year of significant disproportions between productiona dn takeway capacity in Permian.

In these difficult conditions midstream companies both increased their capacity and even faced the need to raise fees for the producers outside the contraced agreements. At the same time a number of companies expanded and boosted capacity of the existing pipelines to cope with the growing demand.

On average (not taking into account fluctuations due to capacity shortage), the Midland, TX to GoM oil price difference narrowed from formerly $30/bbl to just $3/bbl (!). All this is due to massive construction and expansion plans and new pipeline projects in Permian coming to operation in 2019 and especially in 2020-2022.

ASSET MAINTENANCE not just in upstream but also midstream, downstream and in the back office with robotic process automation is yet another success factor. use of IoT approach, focusing on maintenance data analysis allowed midstream companies to control their costs better.

According to Deloitte, the prize is sizeable for global oil and gas companies with the potential to save millions from their combined $2.4 trillion in operating costs.

U.S. is also expected to continue toward growth as an LNG exporter, already having strong refined product exports with gains in natural gas exports, particularly into Mexico.

If you are looking for more information about energy companies, their assets, and energy deals, please, contact our sales office mapping@hartenergy.com, Tel. 619-349-4970 or SCHEDULE A DEMO to learn how Rextag can help you leverage energy data for your business.

Corpus Christi and its O&G Infrastructure

![$data['article']['post_image_alt']](https://images2.rextag.com/public/HEMDS_SiteSupportFiles/BlogImages/Corp_Christi_LNG_Map.png)

Export Opportunities For Permian’s and Takeaway Problem

Additional Contracts For Midland-To-ECHO Pipeline System

![$data['article']['post_image_alt']](https://images2.rextag.com/public/HEMDS_SiteSupportFiles/BlogImages/ECHO_Enterprise.png)

The execution of these additional agreements boosts further total committed volumes. Read details. See it on a map.

![$data['article']['post_image_alt']](https://images2.rextag.com/public/blog/R265_Blog_Williston Basin Overview_ 2022 vs 2023, Bakken Shale, Operators, Deals, 2024 Update.png)

The Williston Basin is a big area filled with layers of rock that sits next to the Rocky Mountains in western North Dakota, eastern Montana, and the southern part of Saskatchewan in Canada. This area covers roughly 110,000 square miles. Geologically, it's very similar to the Alberta Basin in Canada. People started drilling for oil in the Williston Basin back in 1936, and by 1954, most of the land where oil could likely be found was already claimed for drilling. The Bakken Formation with parts of Montana, North Dakota, Saskatchewan, and Manitoba has become one of only ten oil fields globally to yield over 1 million barrels per day (bpd) since the late 2000s. It is currently the third-largest U.S. shale oilfield, behind the Permian and Eagle Ford. The boom in the Bakken started around September 2008, coinciding with the U.S. housing market crash. The application of new technologies, such as swell packers enabling multiple-stage fracturing, significantly enhanced oil recovery, making the Bakken Formation a key player in the U.S. In 2022, the Bakken oil field saw big improvements in how much oil and gas it could produce. At the start of the year, 27 drilling rigs were working there, more than double the 11 rigs from the start of 2021. Important upgrades included making the Tioga Gas Plant able to process 150 million cubic feet more gas each day, and making the Dakota Access Pipeline bigger, increasing its oil transport capacity from 570,000 to 750,000 barrels every day.

![$data['article']['post_image_alt']](https://images2.rextag.com/public/blog/266_Blog_Continental Resources's wells in southern Midland and Ector counties, Texas.png)

Continental Resources is expanding its operations in the Midland Basin, including taking over some assets that used to belong to Occidental Petroleum. The company plans to use its expertise in exploration in this area.

![$data['article']['post_image_alt']](https://images2.rextag.com/public/blog/R267_Blog_EQT and Equinor Swap Marcellus Shale, Strengthen Appalachian Onshore Assets in the US.png)

Equinor and EQT Corporation have agreed that Equinor will exchange its operated assets in the Marcellus and Utica shale formations in Ohio for a stake in EQT’s non-operated interests in the Northern Marcellus formation.