Comprehensive Energy Data Intelligence

Information About Energy Companies, Their Assets, Market Deals, Industry Documents and More...

Appalachian Basin Overview: Marcellus, Utica, Trends, Predictions, 2022 vs 2023

04/11/2024

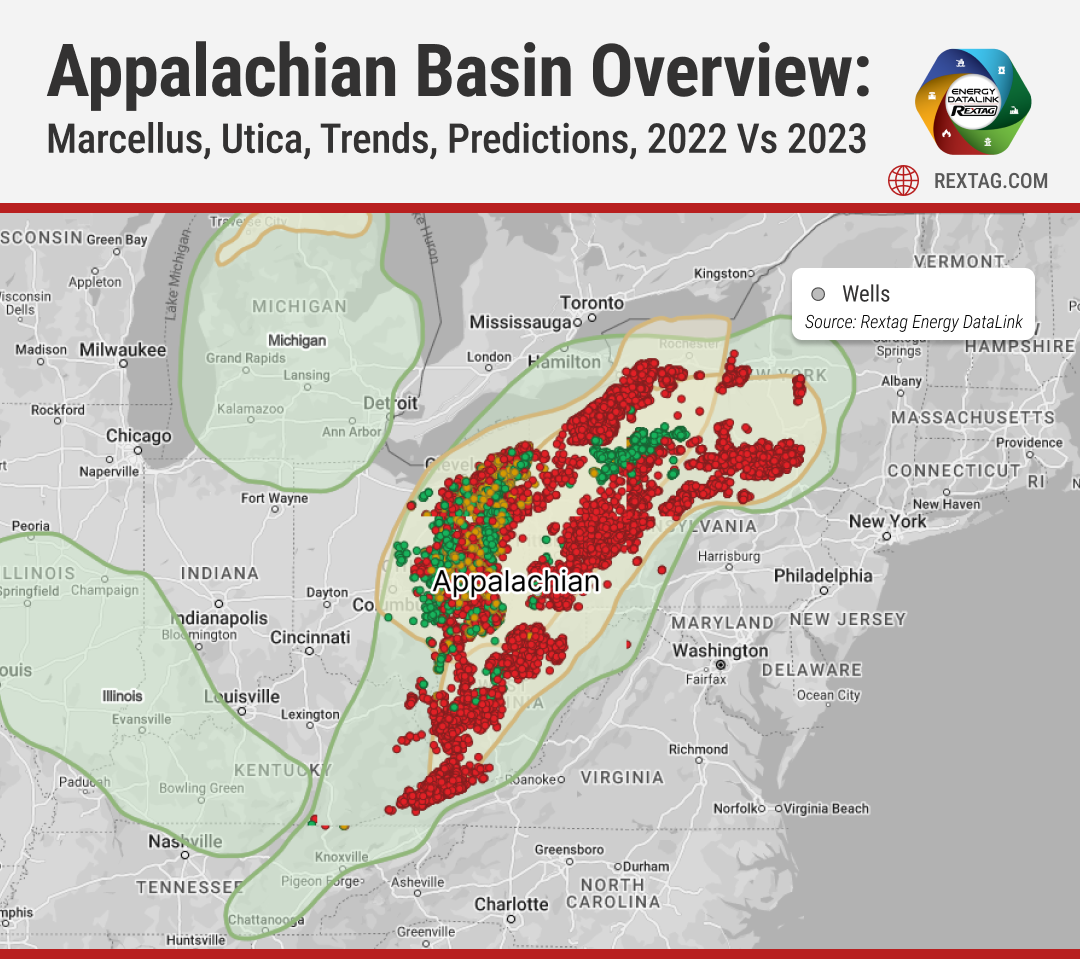

Appalachian Basin (formerly Marcellus and Utica) covers most of New York, Pennsylvania, Eastern Ohio, West Virginia, and Western Maryland in the north, reaching down to parts of Northwest Georgia and Northeast Alabama in the south. The basin is massive, covering about 185,000 square miles, roughly 1,000 miles long from northeast to southwest, and in some places, it's up to 300 miles wide.

In this area, some major companies are making significant investments. EQT stands out as the largest producer in the Appalachian Basin, with other key players including Chesapeake, Range Resources, Antero, Repsol, and Gulfport also actively investing.

Turn Back in Time

One of the most recognized aspects of this region is its coal production. Coal mining has a long-standing history here, spanning over 300 years. The stories of the West Virginia coal mines are especially famous.

When considering the exploration of natural gas and oil, it might seem like a relatively new development in the Basin, especially with the advent of hydraulic fracturing and horizontal drilling, along with all the press surrounding the Marcellus Shale.

However, the truth is, this activity has been happening for a very long time. A particularly fun fact is that the first commercial oil well in the United States was drilled on August 27, 1859, near Titusville, Pennsylvania, known as the Drake Well. For history buffs, this is likely a familiar story. This indicates that oil and natural gas production has deep roots in Appalachia, particularly in Pennsylvania. Even more, natural gas discoveries in the area date back to 1821 in New York State, underscoring that this region is familiar to the energy game. The real change has come from the success of horizontal drilling and hydraulic fracturing techniques, alongside the significant resource plays of the Marcellus and Utica Shales.

In the 1800s, the Drake Well began the quest for more oil across the basins. Early drillers would identify oil by observing surface seeps, indicating underground reserves, hence deciding where to drill based on oil bubbling up to the surface. This method was the primary way oil was found for some time. Until around 1904, the Appalachian Basin was the leading oil-producing region in the U.S., marking it as an early pioneer in the oil and natural gas industry.

Marcellus Shale Play

The Marcellus Shale is recognized as one of the largest natural gas fields in the United States and stands out as the most productive natural gas formation in the Appalachian Basin. Dated to the Middle Devonian period, it is approximately 393 to 382 million years old.

What's fascinating about the Marcellus Shale is its extensive reach across much of the Basin, particularly prevailing in Ohio, West Virginia, Pennsylvania, and New York. However, due to a fracking ban, there is currently no active drilling in New York. Despite this, the Marcellus Shale's presence is undeniable in the state. The US Geological Survey notes that the Marcellus covers about 95,000 square miles of the 185,000 square mile Appalachian Basin, with 72,000 square miles deemed prospective for gas extraction.

Depth-wise, the Marcellus Shale is one of the deeper formations, especially in parts of Pennsylvania where it reaches depths of about 6,000 feet. In contrast, it becomes shallower in Eastern Ohio, dipping to around 2,000 feet. The drilling techniques used are notable for their complexity; wells often start at depths of 6,000 feet, and then drillers steer the wellbore horizontally for a mile or two, resulting in total well lengths that are impressively long.

The Marcellus Shale is North America's largest gas shale formation, accounting for a third of the total U.S. shale gas production. It generates over 25 billion cubic feet (BCF) of natural gas daily. By the beginning of 2024, the Marcellus Shale had yielded 50 trillion standard cubic feet (TSCF) of natural gas, which is the equivalent of 8.3 billion barrels of oil.

EIA in 2015 provided an estimate Proven reserves were 77.2 trillion cubic feet of gas and oil reserves were around 143 million barrels. As of January 2021, the Upper Devonian layer had only 399 producing wells, which, in comparison to the over 15,000 wells drilled in the Middle Devonian Marcellus, contributed a relatively small amount of gas.

Utica Shale

The Utica Shale (beneath the Marcellus Shale) is another key player in natural gas production. Sometimes known as the Point Pleasant Utica Shale formation, it's older and geographically more extensive than the Marcellus due to its deeper placement. This depth makes drilling generally more costly, with wells reaching down between 5,000 and 11,000 feet, where most of the productive activity occurs.

Drilling in the Utica Shale kicked off in Quebec in 2006 and made its way to Ohio by 2011. The formation stretches under a large swath of the northeastern U.S. and parts of Canada, including most of New York, Pennsylvania, Ohio, and West Virginia, and extending into Ontario and Quebec. In certain areas like northwest and central Pennsylvania and northeast and central Ohio, the shale's thickness can exceed 300 feet.

The Utica Shale's potential is vast, harboring around 117 trillion cubic feet of undiscovered, technically recoverable natural gas, alongside 1.8 billion barrels of oil and 985 million barrels of natural gas liquids (NGLs). In 2017, the Energy Information Administration (EIA) pinpointed the proven reserves in the Utica Shale play in Ohio at 6.4 trillion cubic feet. The combined might of the Marcellus and Utica formations in the Appalachian Basin holds about 214 trillion cubic feet of undiscovered, technically recoverable natural gas resources, according to the U.S. Geological Survey (USGS).

Similar to the Eagle Ford formation in South Texas, the Utica Shale features different types of hydrocarbon zones based on how deep it is buried. In the eastern part, it primarily contains dry gas. Closer to the Pennsylvania-Ohio border, where it's not buried as deep, gas liquids are produced. Towards its western side in Ohio, it mainly produces oil.

In terms of oil production from horizontal wells in the Utica Shale, data for the first three quarters of 2023 revealed nearly 20 million barrels were produced. This is about 300,000 barrels more than the total production in 2022 and 3.5 million barrels more than in 2021. Specifically, oil production in Ohio saw a significant increase of 31% in the third quarter of 2023 compared to the same period in 2022.

After acquiring Chesapeake Energy's Ohio Utica Shale assets, Encino Energy became a prominent player in the Utica region. In 2023, the company significantly increased its production of liquids by nearly 35%, reaching 70,000 barrels per day (bbl/d), with a third of this volume being crude oil. Liquids made up 40% of Encino's total daily production, which amounted to 1.1 billion cubic feet of gas equivalent. The company focused 90% of its capital on the oil-rich areas of the Utica Shale, where it drilled the majority of its 55 wells in 2023.

2022

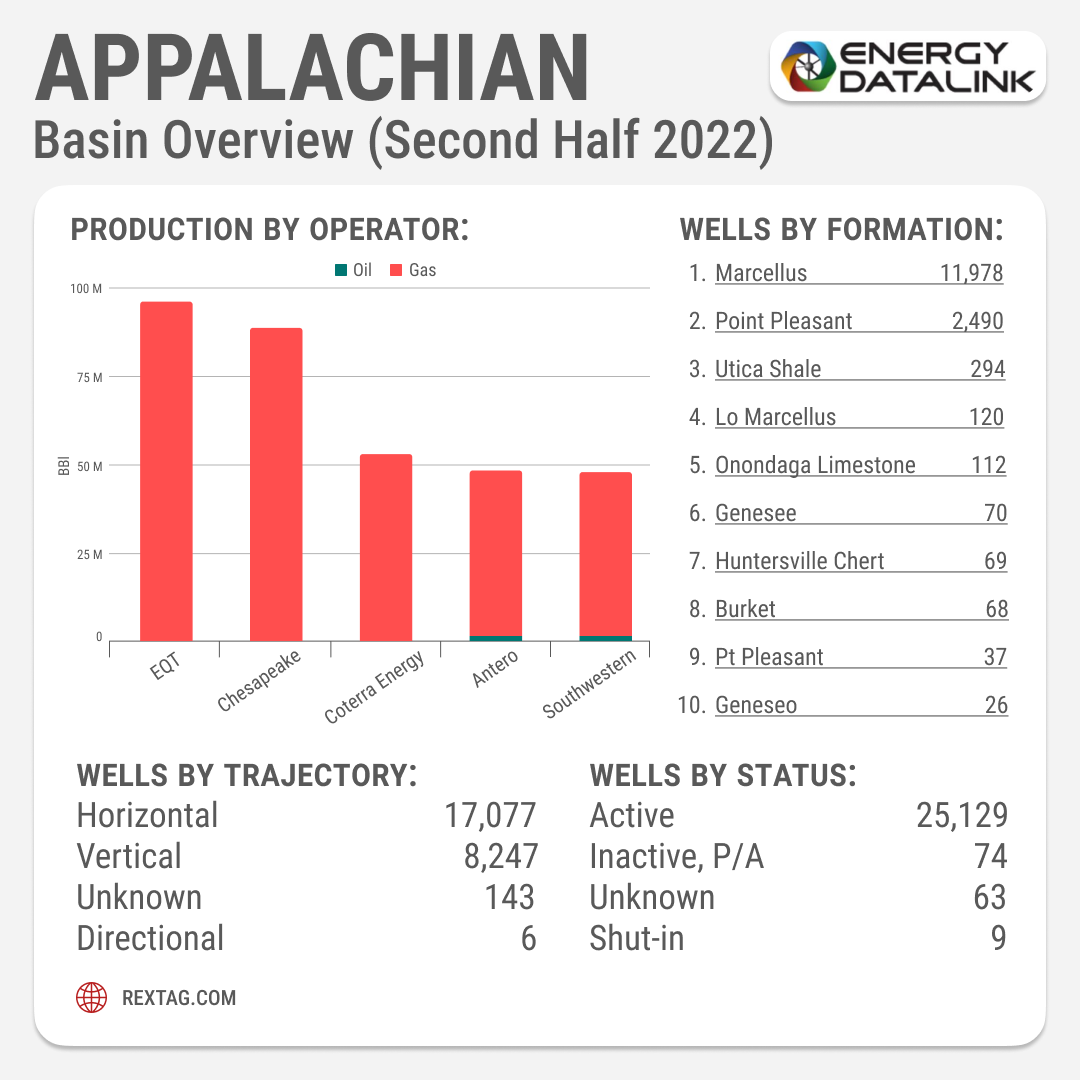

In the second half of 2022, EQT and Chesapeake led the gas production in the Appalachian Basin, with EQT producing over 75 million barrels and Chesapeake just a bit less. Close behind, both Coterra Energy and Antero produced over 50 million barrels of gas. Southwestern was the smallest of the top producers, with about 25 million barrels of gas.

Drilling was most active in the Marcellus Formation, where 11,978 wells were drilled. The Point Pleasant formation had 2,490 wells, and there were far fewer wells in the other formations: 294 in Utica Shale, 120 in Lo Marcellus, 112 in Onondaga Limestone, 70 in Genesee, 69 in Huntersville Chert, 68 in Burkett, 37 in Pt Pleasant, and Geneseo had the fewest at 26 wells.

Most of the wells were horizontal—17,077 in total. Vertical wells were also common, with 8,247 drilled. There were 143 wells with unknown trajectories, and directional drilling was quite rare with only 6.

As for the status of the wells, 25,129 were actively producing, while a small number, 74, were inactive or had been plugged and abandoned. The status of 63 wells was not known, and 9 wells were shut-in and not currently in use.

2023

The overall drilled but uncompleted (DUC) wells in the Appalachian region, including both the Marcellus and Utica plays, saw an increase by May 2023. Specifically, the DUC total in Appalachia rose by 212 wells, a 42.6% increase from the previous year to 710, from 498 one year ago which reflects a growing inventory of wells that could be brought online to boost production.

In June, the number of active drilling rigs decreased, with the Appalachian Basin seeing a 9% drop, which was the smallest after the Permian Basin.

In Q2 2023, the Appalachian Basin was estimated to hold 214 trillion cubic feet of natural gas. The Marcellus-Utica shale alone added 36 billion cubic feet per day to the U.S. natural gas production, doubling its daily output to 35 billion cubic feet in recent years. The region's pipeline capacity was around 24 billion cubic feet per day at the start of 2023. Additionally, the number of active drilling rigs in the area increased by 34%. Daily crude oil production in the Appalachian basin increased by 32.9% in the past year. Other regions also experienced growth, with the Permian rising by 10.3% and the Bakken by 6.4%. Meanwhile, natural gas daily production in the Appalachian basin grew by 1.9% during the same period.

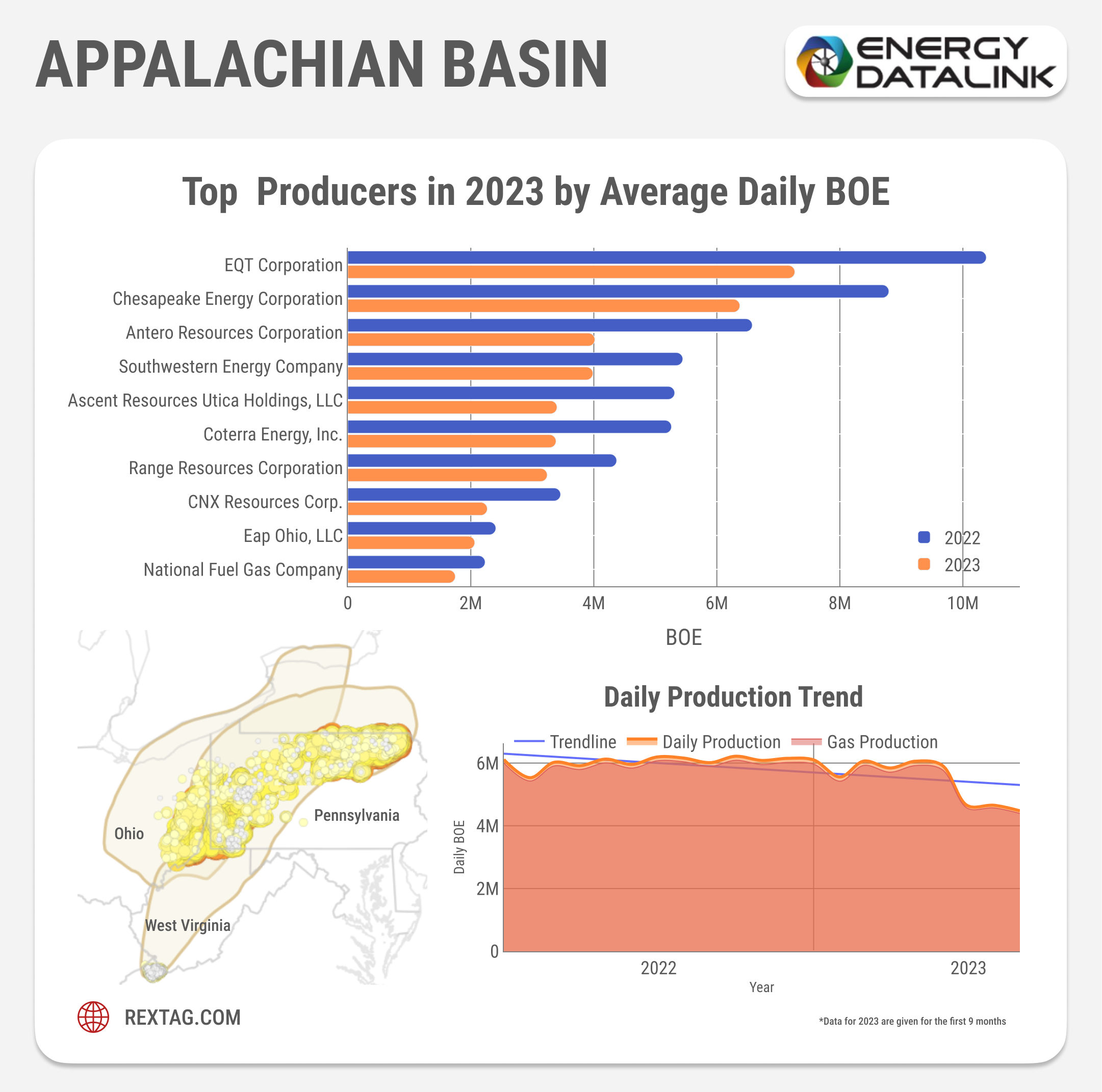

As of June 2023 daily production was reported as follows: Range Resources Corporation produced 342 mboe/d, EQT Corporation - 873 mboe/d, Coterra Energy - 640 mboe/d, Antero Resources Corporation - 551 mboe/d, and Southwestern Energy Company - 764 mboe/d.

In December, a significant storm led to unexpected drops in production, affecting gas supplies to plants. During the Winter Storm Elliott, gas output in the Appalachian Basin's Marcellus and Utica shale formations fell by 23% and 54%, respectively.

Production By Formation for full 2023:

- The Marcellus Formation is the leader in oil and gas production in the Appalachian region, with about 120 million barrels of oil and 72.36 billion cubic feet (Bcf) of gas, totaling around 12,180 MBOE. This formation has the most producing wells at 23,731.

- The Point Pleasant Formation follows with significant output, producing approximately 178 million barrels of oil and 15.01 Bcf of gas, adding up to nearly 2,680 MBOE from 2,879 wells.

- The Utica Shale is contributing as well, with 2.3 million barrels of oil, 1.28 Bcf of gas, and 216 MBOE from 679 wells.

- In the Onondaga Limestone, there's a production of 5.3 million barrels of oil, 1.14 Bcf of gas, and 195 MBOE coming from 2,379 wells.

- The Lo Marcellus is adding 1.27 million barrels of oil and 714.79 Bcf of gas, with a total of 120 MBOE from 158 wells.

- The Clinton Sand has 20.9 million barrels of oil, 350 Bcf of gas, and 79 MBOE from a notable number of 69,110 wells.

- From the Huntersville Chert, there's 1.8 million barrels of oil, 406 Bcf of gas, and approximately 69.5 MBOE from 135 wells.

- The Genesee is producing 44,092 barrels of oil, 404.92 Bcf of gas, and 67.5 MBOE from 245 wells.

- Lastly, the Pt Pleasant adds 52,270 barrels of oil, 330.58 Bcf of gas, and 55.15 MBOE from 39 wells.

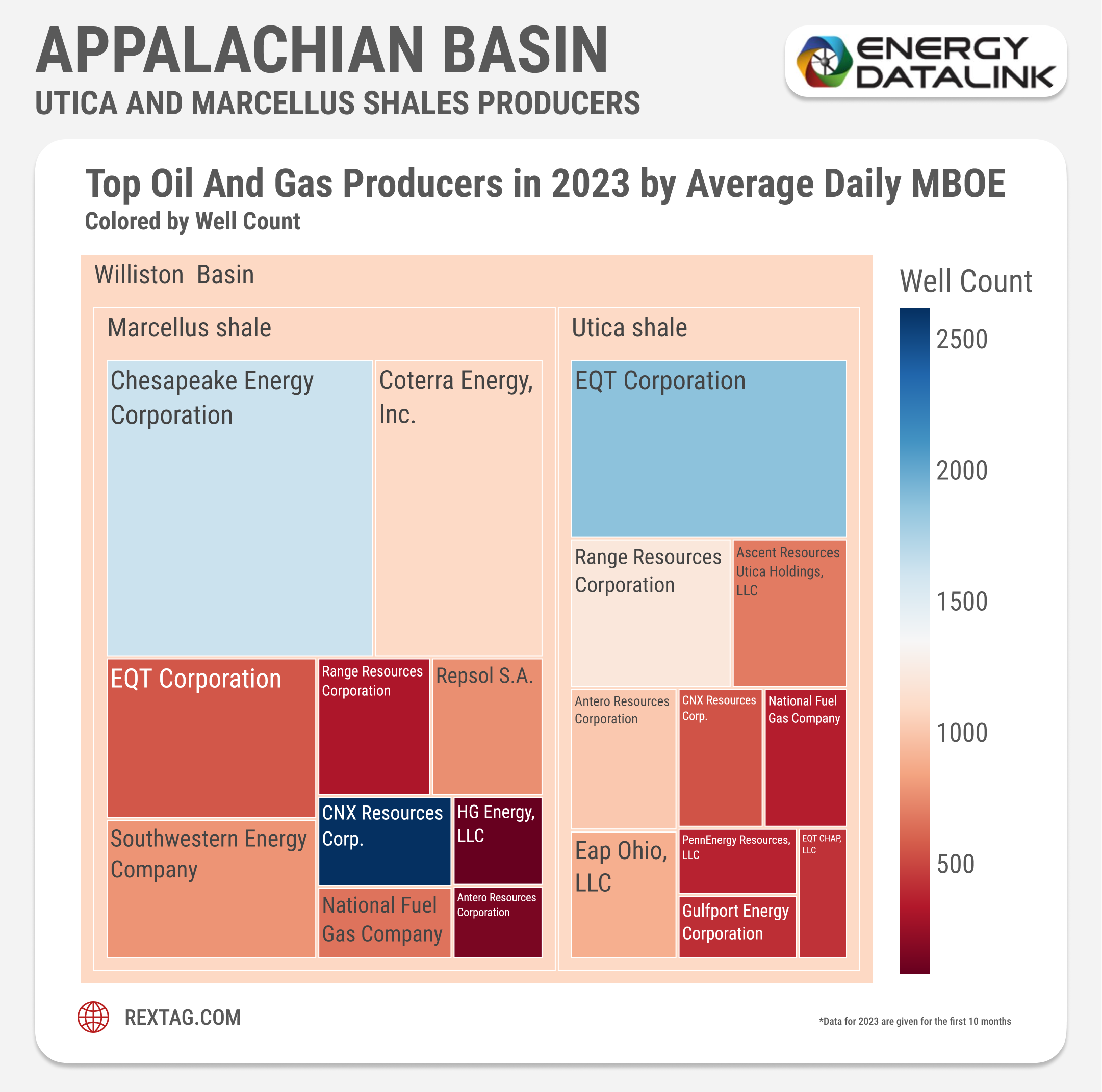

TOP 10 Operators in Appalachian Basin:

- Chesapeake Appalachia had a significant production of around 6.4 million barrels of oil and 10.93 billion cubic feet (Bcf) of gas, totaling approximately 1.83 billion barrels of oil equivalent (BOE), with 7,305 producing wells.

- EQT Production Company produced about 5.1 million barrels of oil, 8.95 Bcf of gas, and 1.5 billion BOE, operating 15,258 wells.

- Antero Resources Corporation stood out with substantial oil production at 36.8 million barrels, 8.68 Bcf of gas, and 1.48 billion BOE from 1,696 wells.

- Coterra Energy had no oil production but reported about 8.61 Bcf of gas and 1.43 billion BOE with 1,099 wells.

- SWN Production Company saw 48.3 million barrels of oil, 7.35 Bcf of gas, and 1.27 billion BOE, with 2,225 wells.

- Range Resources-Appalachia's numbers showed around 41.1 million barrels of oil, 6.54 Bcf of gas, and 1.13 billion BOE from 5,896 wells.

- Ascent Resources Utica Holdings had 54.4 million barrels of oil, 5.18 Bcf of gas, and 917.75 million BOE, operating 929 wells.

- CNX Gas Company produced 3.79 million barrels of oil and 4.74 Bcf of gas, amounting to 793.31 million BOE from 7,225 wells.

- Rice Drilling B showed minimal oil production but had 4.05 Bcf of gas and 674.85 million BOE with 617 wells.

- Chief Oil & Gas recorded no oil but 2.74 Bcf of gas production and 456.79 million BOE from 439 wells.

2022 vs 2023

The Energy Information Administration (EIA) predicted that 2022 will mark the highest point of gas production from the Marcellus and Utica fields in Appalachia, a level not expected to be matched until 2045. At the same time, they forecast that the Haynesville and Permian basins combined will soon produce more natural gas than Appalachia, with their output increasing by over a third by 2050. It's expected that half of this growth will happen in just the next five years.

Because of this, the portion of U.S. natural gas coming from Appalachia is likely to drop from 41.9% in 2022 to 37.2% by 2050.

It appears that gas production in Appalachia, mainly from the Marcellus and Utica basins, started to level off towards the end of 2019. In December 2019, the average monthly production was over 31 billion barrels, 50% more than what was produced by the Permian and Haynesville basins in the Southwest and Gulf Coast combined. However, since then, production in Appalachia has seen minor ups and downs, leading to April 2023's output being almost the same as in December 2019.

During the same timeframe, gas production in the Permian and Haynesville regions continued to increase. By October 2022, the combined output from these areas overtook that of the Appalachian region.

In June 2023 the net acreage for natural gas operations in the Appalachian Basin saw Kentucky with a stable 74% net revenue interest yet a slight drop in acreage to 62,769 from the 2022's 63,009. Virginia and Tennessee kept steady in both net revenue interest, at 83% and 85% respectively, and in net acreage, with Virginia at 4,504 acres and Tennessee at 2,485 acres, unchanged from June 2022.

In 2023, there was a notable shift in production trends between the Appalachian region and the Permian/Haynesville areas, primarily influenced by several factors, including the U.S. natural gas industry's growing focus on exports. At that time, nearly a quarter of U.S. natural gas production was being sent abroad, with expectations for this figure to continue rising. The Permian and Haynesville regions, due to their proximity to Gulf Coast export facilities, were well-positioned to meet the increasing demand from Europe and Asia.

Conversely, production in the Appalachian region was limited by the lack of sufficient pipeline capacity to transport gas to export terminals on the East Coast or other regions of the U.S. This bottleneck prevented the region from fully capitalizing on export opportunities, thereby directing more natural gas from the Southwest and Gulf Coast towards international markets. The situation was expected to see a slight improvement with the completion of the Mountain Valley Pipeline (MVP), which had recently received support from the Fiscal Responsibility Act. The MVP, capable of transporting 2.2 billion cubic feet of gas per day, represented about 7% of the Appalachian production at that time. However, since not all gas transported by the MVP would be new to the market, its actual impact on Appalachian production levels was anticipated to be less than 7%.

Main Challenges

One of the big plus points for the Appalachian Basin is its location near the Eastern Seaboard and big markets like New York and New England. However, fluctuating commodity prices pose a significant risk, making the financial side of things a major challenge for companies operating there.

Right now, there's a drop in the production of associated gas because of the shutting down and reduced drilling of oil wells, especially in major areas like the Permian and Appalachian Basin. This situation has helped prop up gas prices temporarily. Despite this, the prices aren't high enough yet to spark a new wave of production or drilling in the Appalachian Basin. Many companies believe that gas prices need to rise above $2.50 per MMBtu for a real investment push in drilling.

The depth of the wells and the extensive infrastructure required to transport gas are significant factors in the region's natural gas and oil production. Additionally, political risk poses a challenge, notably the fracking ban implemented in New York in 2010. Although there is some production from wells drilled before this ban, the bulk of today's production is driven by Pennsylvania, Ohio, and West Virginia.

Despite the proximity of these production areas to major markets like New York and Boston, transporting gas to these locations is fraught with difficulty. A key issue is the lack of permit approvals in New York for new pipelines, exemplified by the Constitution pipeline. Despite receiving the green light from the Federal Energy Regulatory Commission in 2014, it has faced delays in New York, impacting the ability to construct and operate the pipeline.

From a geological perspective, the risk is considered low. Drilling in the area has provided a solid understanding of the play's characteristics, such as depth and potential yield. The main concern, however, is economic viability. The presence and location of gas are well known but exploiting these resources at current prices may not be financially feasible.

Infrastructure-wise, a significant challenge is midstream capacity. As new wells are drilled, the existing infrastructure nears or reaches capacity, necessitating expansion. While this isn't a major problem in producing areas like parts of Pennsylvania, the primary issue lies in transporting the gas from local areas to major hubs and markets, particularly securing approval for export pipelines.

Current Trends and Predictions

The Energy Information Administration (EIA) predicts that by the year 2050, gas production in the Appalachian Basin might hit 50 billion cubic feet (BCF) a day. This figure would surpass the gas output of many countries, which is pretty astounding when you think about how long this area has already been producing gas and the vast amount of untapped potential that remains.

One significant boost to demand in the region is the construction of Shell's massive ethane cracker in Pennsylvania. This facility, which has been years in the making, is expected to reach an average peak annual production of 1.6 million tons of polyethylene. It's a major development, set to consume a substantial amount of gas for the production of feedstock used in chemicals and plastics, providing a local outlet for gas utilization.

The transition from coal to natural gas is another factor expected to uplift natural gas prices over the long term. The demand for natural gas, especially in the Appalachian basin, is on the rise due to such shifts. Forbes notes that natural gas is the only fossil fuel projected to see an increase in global demand through 2035. The expansion of LNG export capacity in the U.S. is anticipated to contribute to price stability and offer some relief to domestic producers. The export capacity is expected to surge to 34 BCF per day by 2027, which should, in turn, elevate prices as this additional capacity becomes operational, especially with global gas prices forecasted to average around $7 per MCF in the future.

Currently, the market is experiencing low prices, but the landscape looks set to change significantly in the next decade. For those holding minerals in Appalachia, patience could yield substantial benefits in the long run. An interesting observation is the broader shift from coal to more environmentally friendly energy sources like natural gas and renewables. Bloomberg emphasized the move away from "dirty coal" towards these cleaner alternatives, highlighting natural gas as the most environmentally friendly fossil fuel. This shift is poised to be advantageous for the natural gas sector.

Moreover, global demand for natural gas is expected to continue growing, positioning the U.S. to lead in LNG exports. By capitalizing on higher global gas prices, compared to the oversupply-driven lower prices domestically, the U.S. has the opportunity to meet and satisfy this increasing international demand.

If you are looking for more information about energy companies, their assets, and energy deals, please, contact our sales office mapping@hartenergy.com, Tel. 619-349-4970 or SCHEDULE A DEMO to learn how Rextag can help you leverage energy data for your business.

EQT and Equinor Swap Marcellus and Utica Shale, Strengthen Appalachian Onshore Assets in the US

![$data['article']['post_image_alt']](https://images2.rextag.com/public/blog/R267_Blog_EQT and Equinor Swap Marcellus Shale, Strengthen Appalachian Onshore Assets in the US.png)

Equinor and EQT Corporation have agreed that Equinor will exchange its operated assets in the Marcellus and Utica shale formations in Ohio for a stake in EQT’s non-operated interests in the Northern Marcellus formation.

Exploring ESG in Upstream Operations: Examining Achievements, Obstacles, and Emerging Patterns

![$data['article']['post_image_alt']](https://images2.rextag.com/public/blog/R130_B_Exploring_ESG_in_Upstream_Operations .png)

ESG considerations are becoming increasingly essential for companies operating in the upstream sector. Failure to address ESG concerns may result in financial and reputational risks, given the growing focus from investors, regulators, and other stakeholders. Companies must prioritize ESG performance and engage with stakeholders to address concerns and mitigate risks. By doing so, they can improve their reputation, attract investment, and contribute to a more sustainable future

![$data['article']['post_image_alt']](https://images2.rextag.com/public/blog/328_Blog_Why Are Oil Giants Backing Away from Green Energy Exxon Mobil, BP, Shell and more .jpg)

As world leaders gather at the COP29 climate summit, a surprising trend is emerging: some of the biggest oil companies are scaling back their renewable energy efforts. Why? The answer is simple—profits. Fossil fuels deliver higher returns than renewables, reshaping priorities across the energy industry.

![$data['article']['post_image_alt']](https://images2.rextag.com/public/blog/327_Blog_Oil Market Outlook A Year of Growth but Slower Than Before.jpg)

The global oil market is full of potential but also fraught with challenges. Demand and production are climbing to impressive levels, yet prices remain surprisingly low. What’s driving these mixed signals, and what role does the U.S. play?

![$data['article']['post_image_alt']](https://images2.rextag.com/public/blog/326_Blog_USA Estimated Annual Rail CO2 Emissions 2035.jpg)

Shell overturned a landmark court order demanding it cut emissions by nearly half. Is this a victory for Big Oil or just a delay in the climate accountability movement?