Comprehensive Energy Data Intelligence

Information About Energy Companies, Their Assets, Market Deals, Industry Documents and More...

U.S. Oil and Gas Drilling 2023-2024 Report: Rigs, Onshore, Offshore Activity, Biggest Companies

03/11/2024

In January 2024, the United States saw a mix of ups and downs in the number of active drilling rigs across its major oil shale regions and states.

Starting with the shale regions, the Permian Basin led with a slight increase, reaching 310 rigs, which is 3 more than in December. The Eagle Ford in East Texas held steady with 54 rigs, unchanged from the previous month. Meanwhile, both the Haynesville and Anadarko regions saw a decrease by 2 rigs each, landing at 42 rigs. The Niobrara faced a larger drop, losing 4 rigs to settle at 27. On a brighter note, the Williston Basin and the Appalachian region saw increases of 2 and 1 rigs, respectively, resulting in counts of 34 and 41 rigs.

Looking at the rig counts by state, the Bakken Region had a total of 32 rigs, mostly in North Dakota. The Rocky Mountain area had 141 rigs, with New Mexico leading the pack. Central Plains had all 44 rigs in Oklahoma, leaving Kansas and Arkansas without any active rigs. The Gulf States had a total of 42 rigs, with Louisiana contributing the most. Texas dominated the count with 304 rigs, especially in District 8 which alone had 176 rigs. Lastly, the Appalachian region had 40 rigs spread across Ohio, Pennsylvania, and West Virginia.

February 2024 Report

In the week leading up to February 16, the industry slowed down slightly, with the total number of active drilling rigs for oil and gas in the U.S. dropping by 2 to 621. This represented a significant decrease from 760 rigs active the same time the previous year. Oil rigs specifically saw a reduction by 2 to 497, while gas rigs remained steady at 121. Despite these decreases, U.S. crude oil production maintained its record-high average of 13.3 million barrels per day (bpd). Additionally, the Frac Spread Count, which estimates the number of crews completing unfinished wells, rose by 10 to 260 for the week. In terms of regional activity, the Permian Basin lost 1 rig, while the Eagle Ford Shale's count remained unchanged.

As reported on February 23, the total rig count rose by 5 to 626, though it was still lower than the 753 rigs operational the same time last year. The number of oil rigs increased by 6 to 503, despite being down by 97 rigs year-over-year. The number of gas rigs decreased slightly by 1 to 120. U.S. crude oil production continued at an all-time high of 13.3 million bpd. The Frac Spread Count also increased by 4 to 264, indicating a rise in well completions. The Permian Basin experienced growth with a 2-rig gain, contrasting with its performance the previous week, while the Eagle Ford maintained its rig count.

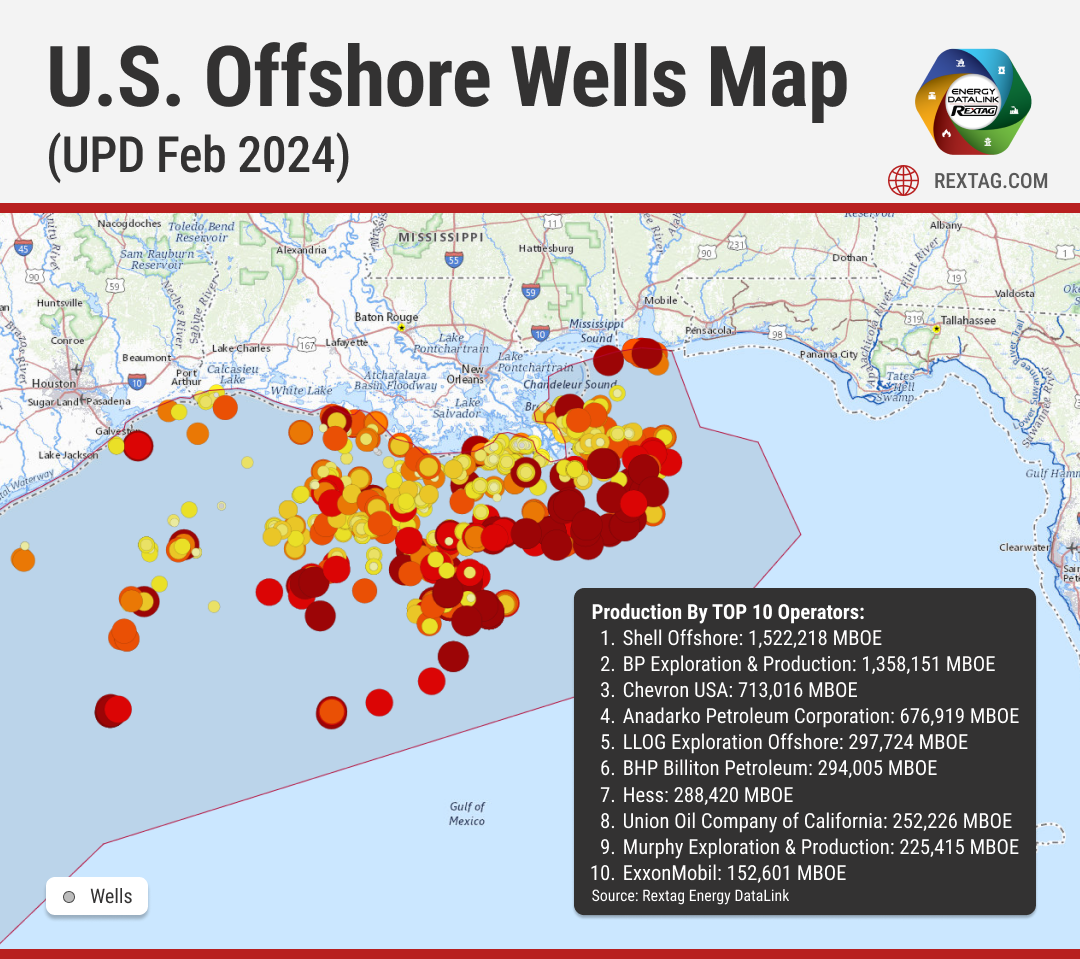

Offshore and Onshore U.S. Drilling

Historically, most U.S. offshore drilling has occurred off Louisiana, Texas, California, and Alaska coasts. The Gulf of Mexico, particularly the western and central parts, is one of the major petroleum-producing areas, contributing significantly to the nation's oil and natural gas output. Major fields in the Gulf include the Atlantis Oil Field and the Tiber oilfield among others.

For U.S. offshore activities, global mobile offshore drilling units (MODUs) experienced growth for the first time since 2014, with the available fleet reporting 622 rigs, an increase from the previous year. This growth is attributed to a stable and healthy oil price, encouraging both fleet sizes and utilization to grow across all international regions.

Interestingly, a shift occurred for drillships, with South America, particularly Brazil and Guyana, becoming the largest region, overtaking the US Gulf of Mexico. The total number of active MODUs during the 2023 census period was 490, marking the highest number since 2016 and indicating a robust utilization rate of 79%, the highest since 2015.

Onshore in the US, rig activity experienced a notable decrease in 2023 to 677 from 893 in the prior year. The Permian Basin saw a sharp drop in its active rig count from 370 to 268. Despite this reduction, the US offshore fleet utilization remained relatively stable, with a slight increase in utilization rates. The drillship segment, in particular, maintained high utilization at 95%.

For onshore drilling, Patterson-UTI Energy Inc. leads with a market capitalization of $4.52 billion as of January 1, 2024, followed by Helmerich & Payne, Inc. with $3.63 billion. These companies are part of the larger landscape of US drilling companies.

New-well oil production per rig saw slight increases in regions such as the Bakken and Eagle Ford, indicating improvements in drilling efficiency and productivity. Similarly, gas production per rig increased in areas like Appalachia and Haynesville.

Gulf of Mexico Offshore Drilling

The offshore drilling sector in the Gulf of Mexico (GOM) is experiencing a tightening market with increasing day rates. This trend is driven by a combination of factors, including longer contract durations not seen in years, rising day rates, and upstream customers seeking to secure rigs well in advance of projected work starts.

The rig count in the U.S. Gulf of Mexico is forecast to remain stable, with 25 rigs both for this year and next. Utilization rates are also expected to stay at the same level – 87% – before moving up to 92% in 2027 as fewer rigs become available in the region. This stability reflects a balanced market, with a mix of supermajors and independents utilizing rigs on both short-term and longer-term contracts.

Jackup day rates in the Gulf of Mexico are anticipated to see upward movement in the coming year as demand remains strong and long-term contracts are handed out. By the second half of 2024, premium jackups could fetch between $120,000/day and $170,000/day, while vintage/standard jackups could net between $80,000/day and $115,000/day.

Biggest U.S. Offshore Oil Rig Companies

- Franklin Howard International

Franklin Howard International specializes in supporting the oil and gas sector with a comprehensive suite of services for rig infrastructure. They offer products for drilling, complete rig setups, and essential spare parts. The company's expertise spans the construction, maintenance, installation, and decommissioning of rigs, including subsea operations and well abandonment.

- Nabors Industries

Operating in around 20 countries, Nabors Industries boasts one of the world's largest land-based drilling rig fleets and provides offshore rigs too. Their offerings include directional drilling, and drilling software, along with automation solutions like the Smart Suite Drilling Automation and ROCKit.

Nabors Industries reported Q4 2023 operating revenues of $726 million, with a net loss of $17 million. This represents an improvement from a $49 million net loss in the third quarter. For the full year, revenues were $3.0 billion, a 13% increase from the previous year. Adjusted EBITDA for 2023 was $915 million, showing a significant growth of 29% year-on-year. These results reflect growth across all company segments, including a 24% expansion in both Nabors Drilling Solutions and Rig Technologies.

- Coastal Drilling Company

Coastal Drilling Company operates in the South Louisiana and Gulf Coast markets, focusing on oil field personnel transportation. Their operations span various locations, including Venice, Port Sulphur, and Morgan City, among others. The company manages a fleet of passenger vessels, including Duke, Mr. Mack, Rolling Thunder, and Scooter, all constructed from aluminum.

- Schlumberger Limited (SLB)

Schlumberger Limited's work includes studying the earth through seismic services, analyzing wellbores, and focusing on sustainability to reach zero emissions and find new energy sources.

In Q1 2023, Schlumberger Limited saw a 32% revenue increase in North America and a 29% rise internationally, driven by higher drilling and sales. Despite some declines, overall growth was strong. In Q2 2023, their revenue rose by 20% to $8.10 billion, thanks to strong international and offshore activities, including in the Middle East & Asia and the Gulf of Mexico. Their profit increased by 8% to $1.03 billion, with adjusted EBITDA up by 28% to $1.96 billion. In Q3 2023, revenue went up by 3%, showing particular strength in the Middle East & Asia and offshore sectors. Year-to-date, revenue grew by 22%, and they launched the OneSubsea joint venture, aiming for innovation in subsea production.

- Halliburton Company

Halliburton Company offerings span various sectors including drilling, formation evaluation, well construction, and completions.

In 2023, Halliburton Company saw impressive growth. In Q1 2023 Profit was $651 million, and revenue hit $5.7 billion, up 33% year-over-year. Q2 2023: Profit reached $610 million, with revenue slightly up at $5.8 billion. Earnings per share increased by over 50%, driven by more global sales, higher activity in North America, and better performance in the Gulf of Mexico. Q3 2023: The company's profit rose to $716 million, with steady revenue at $5.8 billion and a 17% year-on-year increase in international revenue. Ending the year, Halliburton reported a profit of $661 million and $5.7 billion in revenue, a 13% rise in annual revenue to $23.0 billion, the highest operating margins in over a decade.

- Baker Hughes Company

Baker Hughes Company solutions range from advanced drilling motors and rotary steerable to innovative automation technologies.

For 2023, Baker Hughes Company demonstrated remarkable growth - 18% increase in revenue to $5.716 billion in Q1, climbing to $6.835 billion by Q4. The company grew thanks to big deals, like CO2 projects for Petrobras and a clean ammonia plant in the U.S. Their earnings from operations started at $438 million, jumping 57% from last year, reached $714 million at its peak, and ended at $651 million. Baker Hughes increased sales in both traditional oilfield services and new energy projects, including hydrogen and blue ammonia. By the end of the year, their adjusted income from operations was up 14% from the previous quarter and 18% higher than the previous year.

If you are looking for more information about energy companies, their assets, and energy deals, please, contact our sales office mapping@hartenergy.com, Tel. 619-349-4970 or SCHEDULE A DEMO to learn how Rextag can help you leverage energy data for your business.

Kinder Morgan Overview: 2022 vs 2023, Oil & Gas Wells, Pipelines, Terminals, Deals

![$data['article']['post_image_alt']](https://images2.rextag.com/public/blog/R264_Blog_Kinder Morgan Overview_ 2022 vs 2023, Oil & Gas Wells, Pipelines, Terminals, Deals.png)

Kinder Morgan stands as North America's top independent mover of petroleum products with around 2.4 million barrels daily across the continent. The bulk of this flow happens through its Products Pipelines division, which navigates gasoline, jet fuel, diesel, crude oil, and condensate through a network of about 9,500 miles of pipelines. Alongside, the company maintains roughly 65 liquid terminals that not only store these fuels but also blend in ethanol and biofuels for a green touch.

Who's Next after Diamondback? Potential Takeover Targets in the Permian Basin

![$data['article']['post_image_alt']](https://images2.rextag.com/public/blog/239_Blog_Who's Next after Diamondback_ Potential Takeover Targets in the Permian Basin.png)

The $26 billion purchase of Endeavor Energy Resources by Diamondback Energy, with its stock up 2.6%, is the newest big deal combining oil and gas production in the Permian Basin under a few big companies

![$data['article']['post_image_alt']](https://images2.rextag.com/public/blog/321_Blog_ Permian Basin Gas Production Pushes Limits – Infrastructure Expansion Needed.jpg)

The rapid growth of natural gas production in the Permian Basin is pushing existing infrastructure to its limits, and additional pipeline projects are on the horizon to meet rising demand, according to East Daley Analytics. Despite ongoing price volatility—marked by repeated declines—demand for expanded energy markets continues to surge.

![$data['article']['post_image_alt']](https://images2.rextag.com/public/blog/320_Blog_Virginia's Renewable Future Dominion Energy Sells Wind Stake for $2.6B.jpg)

Dominion Energy has struck a major deal by selling half of its stake in the Coastal Virginia Offshore Wind (CVOW) project to Stonepeak, one of the world’s leading infrastructure investors, for $2.6 billion. While Dominion will retain full control over the project’s development and day-to-day operations, this partnership gives Stonepeak a non-controlling 50% interest.

![$data['article']['post_image_alt']](https://images2.rextag.com/public/blog/319_Blog_ Turning Trash into Treasure Are Landfills America’s Next Green Energy Source.jpg)

Landfills are essential to America’s waste management system, yet they face several operational, environmental, and regulatory challenges. With over 2600 active municipal solid waste (MSW) landfills across the country, they occupy an average of more than 600 acres, which is roughly equivalent to 500 football fields. Methane emissions from landfills contribute significantly to global warming, accounting for 15.1% of U.S. methane emissions. As the waste sector is a major contributor to methane emissions, there is a growing emphasis on improved monitoring, reduction technologies, and the integration of renewable natural gas (RNG) solutions to mitigate the impacts of these emissions.