At Hart Energy's recent DUG East/Marcellus-Utica Midstream Conference, Rystad's analysts raised the possibility that Appalachia's natural gas production can actually be maintained or even increased without the significant investment in wells of the past.

As per Rystad's projection, natural gas prices will stay around $3-$4 per MMBtu all the way to 2030, which is a good point for economic feasibility at the asset level. The U.S. will also be able to stay a key player in energy supplies in the long run because of this.

It is inevitable: gas will replace coal in the power generation fuel mix because of the energy transition to electrification and lower emissions goals. At the moment, the coal industry dominates the power generation mix in Asia, including Australia, where coal produces 45% of electricity. This creates opportunities for natural gas, which won't be covered fully by local resources, leaving a possibility for import.

Despite the energy struggles of 2021, the importance of gas in the energy system has been reinforced. There is a potential for more energy crises to arise in the future, depending on when and how quickly the energy transition happens. Thus, to meet power demand and avoid emissions of greenhouse gasses, regions such as Europe and Asia need greater amounts of LNG. There will be intense competition between U.S. and Russian producers in those markets, but the U.S. maintains a supply advantage, while Russia will see its share of the market decline notably from the mid-2030s to 2050.

By the early 2040s, LNG demand will likely peak at 718 metric tons. But in the short term, the LNG market is relatively tight and unable to fulfill such needs, because U.S. export terminals have not yet been built. LNG export terminal projects must be completed promptly if the supply target of 700+ metric tonnes is to be reached by 2040.

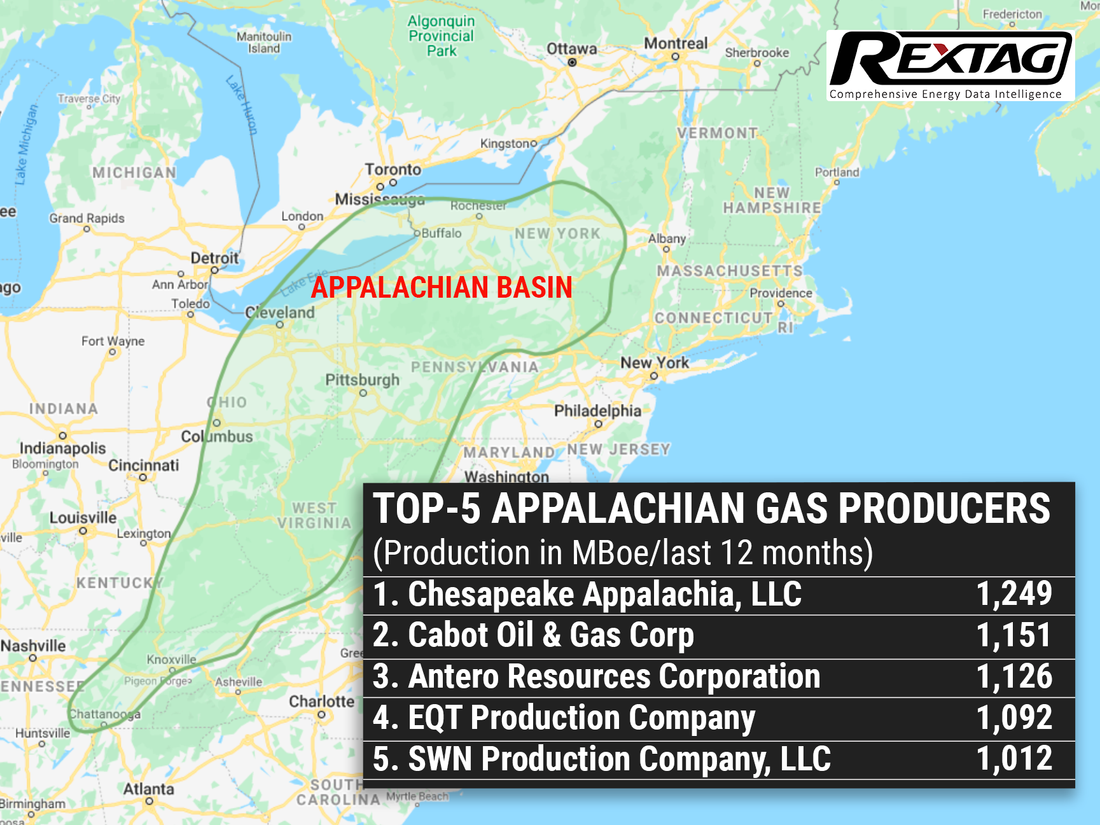

It becomes quite important to consider the production capabilities of Appalachian producers in that context. Historically, productivity has ranged between 1 and 2 Bcf/d from 2014-to 2016, plateaued at around 2 Bcf/d in 2019, and then increased to 2 to 2.4 Bcf/d in 2020 and then started rising again in 2021. And the curves appear to be sustainable.

And it isn't only because operators are drilling better acreage that productivity gains have been stable. During 2016-2017, Tier 1 and Tier 2 locations produced lower output, implying that this learning curve continues to be steep and that the operators are actually realizing these capital efficiency gains.

The takeaway and regulatory constraints of the Northeast region are not to be ignored, but even if those obstacles impede Appalachia's growth at the same rate as the Permian or Haynesville, it does not detract from the value of the Marcellus and Utica basins.

The Appalachians will still be the top producers at a very competitive pace as long as commercial inventory exists. After all, as long as there is commercial inventory, somebody will have to drill.